It's week 2 of the challenge and we are moving right along. We're still in the kitchen this week but we will re-focus our efforts towards organizing our food & the pantry. If you don't have a pantry (like me), organize the area where you keep your food. If you didn't get your refrigerator cleaned out last week, do it now. You have 7 days to complete the second challenge but shouldn't take you that long. Be quick and efficient with your time. If you would like to purchase any of the items featured in this post, check out my favorites shop here. FIRST TIME PARTICIPANTS: Welcome! We are glad you're here. Take a minute to look over the challenge details then begin working at your own pace. You can find the week 1 challenge here. Before you start, print out the complete 14 week schedule and checklists below.   Welcome to week 2 of the challenge. We will be spending the next 7 days deep cleaning and organizing the pantry (or the area where you keep your food). For encouragement, join our Home Organization Facebook community to share your progress, or struggles, or questions. Or simply look through the photos and read how others are doing. This week should be pretty straight forward. Empty the pantry, wipe it out, toss expired food, and put it all back in an organized fashion. THE PROCESS

We do not have a pantry in our new home. It just wasn't important to me. From my experience, having a pantry meant a lot of expired food (because I bought too much and we didn't eat it in time) and excess clutter. I also shop for groceries every Sunday so I don't need to store too much more than a week or 2 of food.  This time around, I made plans to use a small cabinet to store food. It's in the hallway right outside of our kitchen. I also have huge 10 foot island that has the storage space I need for small appliances, canned goods, etc… so it works well for us. Each week after I return from the grocery store, I spend a couple of minutes tidying up the cabinets. It has helped me to eliminate wasteful food and indulgent grocery shopping. I try to stick with a list and only buy what we need for the week. It's been a nice change from the overstuffed shelves full of food. THE LAYOUT. No matter if you have a large pantry or small set of cabinets, categorize your food storage into zones for easy access and order.  DRY GOODS. Glass jars with airtight lids are the perfect way to condense boxes and bags into uniform food storage. These jars are my favorite. You can also store dry goods in OXO containers or mason jars. Use a labeling machine to label the jars.  If you don't have a labeler, you can use a wet erase marker and write on the glass jar.  BASKETS. Wicker baskets & bins are great for storing potatoes, onions, bagged items, and cutting boards. It's also easy to grab what you need quickly.   CANNED GOODS. We keep our canned goods in the cabinet under our kitchen island. I am grateful for this extra space.  There's not much pretty organization involved down here. Everything is placed into categories and that works for us.  Another way to organize canned goods is by using narrow bins. Here is a photo of my canned goods in our old pantry. You can see more detailed photos here. The bins are from The Container Store.  DECOR. Not only can your pantry be functional but it can be pretty as well. Bring your home decor into the pantry and add a little charm. I love to display vintage bread boards and Demi John jars. I also keep my French apron & dried lavender hanging on the sides of the cabinet.    Here are several blog posts that are sure to inspire you to get your pantry organized.

For the perfect companion guide to our challenge, purchase The Complete Book to Home Organization. It includes all 14 weekly challenges and will be your guide over the next 14 weeks, as you tackle your spaces. No need to log onto the computer for ideas, this manual has it all!  For help with cleaning your house during the challenge, be sure to get the complimenting book The Complete Book of Clean. It has tons of cleaning recipes, tips, and checklists that will teach you how to get your homes sparkling clean.  Concentrate on purging your pantry this week. Follow the process I've laid out for you. Make sure to set up organized zones for better functionality. If. you need more guidance, be sure to get my book. Try not to get side-tracked and don't move ahead until you are completely finished with the space. Share your progress on Instagram using the hash tag #abfolchallenge, blog about the weekly challenges, and share your before and after pictures over at my Home Organization FB group here. Hold yourself accountable and finish all 14 challenges! I can't wait to see what you accomplish. Good luck. I'll see you back next week for the week 3 challenge. Happy Organizing! ~Toni

0 Comments

Finishing the basement in your home is a great way to maximize the space you already have, without having to add on any square footage in the form of an addition. Whether you want to go the more luxurious route and turn your basement into a home theater, or you're simply looking for a way to create more living space in your home, finishing your basement is a great way to do so. However, there are a few things you'll want to keep in mind for a successful basement remodel. Below, we cover 5 tips to get you started.  For many, buying a home is a dream come true. However, if you've been through the process, you know it's not an easy task. You must figure out how much you can afford, get pre-approved, make an offer, and get a home inspection.  Grain-free cassava flour tortillas requiring only three ingredients! These homemade tortillas are easy to make and are paleo and AIP-friendly. If you enjoy all the foods that involve tortillas – tacos, burritos, wraps, enchiladas, etc – but have a difficult ... The post Cassava Flour Tortillas (Paleo, AIP) appeared first on The Roasted Root. This is a repurposed-repurposed project. I love it when that happens!  Click here to read the rest of this post... We get asked a lot of questions about exterior painting preparation tips. There's nothing like a vibrant, fresh coat of paint to enhance the appearance of your home. A clean, new coat of paint looks great, even if you're simply replacing the old color or style with the same type. In many cases, repainting begins with stripping off the old layer in preparation. That smooth, newly repainted look depends on having a smooth, prepared surface to start from. Here are some situations in which old paint needs to be stripped off:

Painting your home is a big job, and it's important that the house be prepared beforehand to allow for many years of new, beautiful paint. The Painting Group, the most trusted painting contractor in Marietta, has received high praise for our professionalism and expertise. Call us today at (770) 818-9885 to learn more about our painting experience. You can also visit us online for details about the staining and painting services we offer for both residential and commercial buildings. The post Exterior Painting Preparation Tips appeared first on The Painting Group. You might be wondering what happens to bed bugs in the winter. The answer is; nothing. Bed bugs are not pests that fall prey to cold weather and die off, nor do they hibernate. While they don't necessarily like cold temperatures, they can survive and continue to move from one location to another, causing infestations as they breed. If you discover you have a bed bug infestation, or just suspect that a bug you've seen in your house is a bed bug, there is no need to panic. Bed bug treatments are available to rid your Souderton home of bed bugs no matter the season.

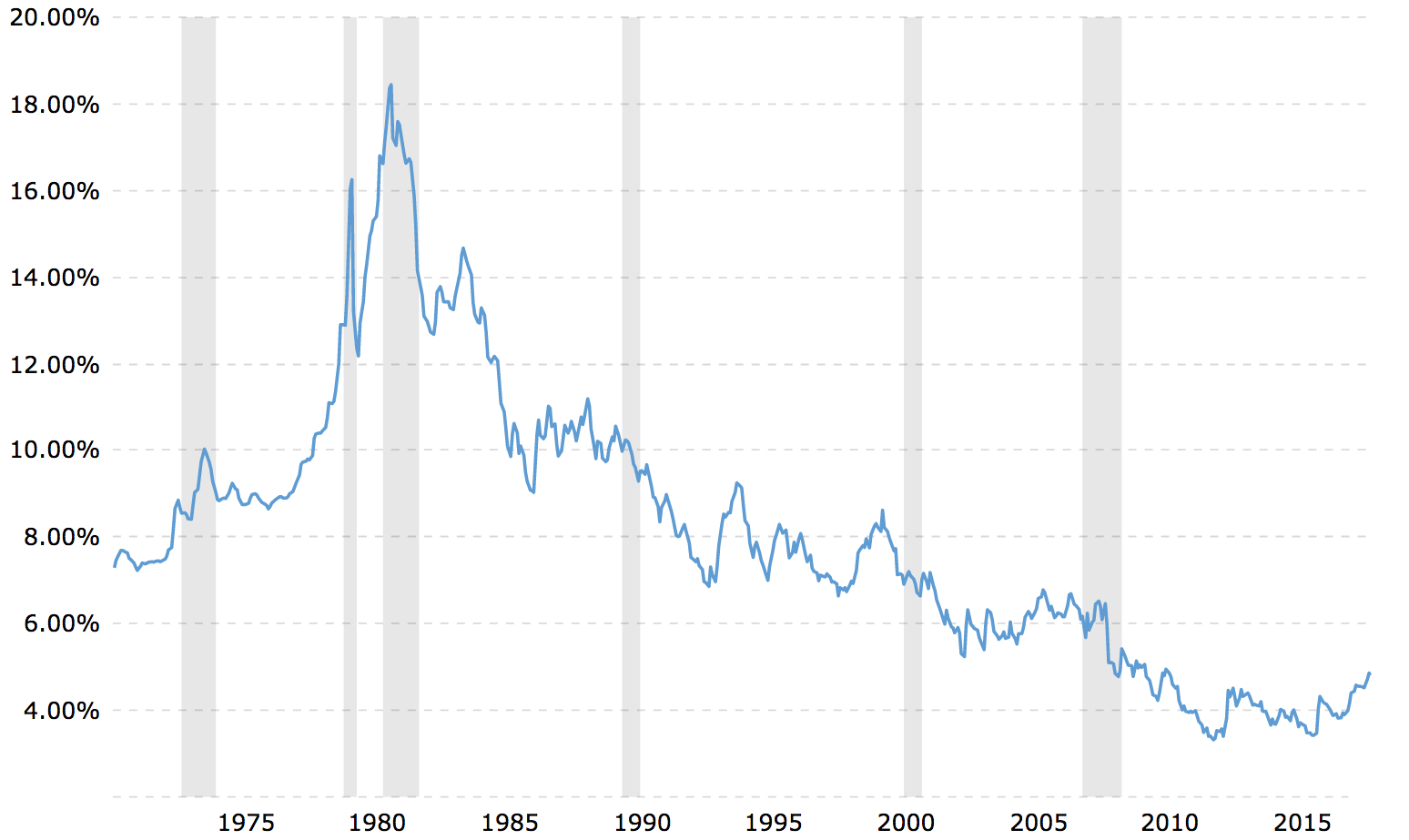

Instead, I got something better. It was letter from my bank saying my adjustable rate mortgage interest rate is going up! This is the first time I've ever received such a letter because, in the past, I would always refinance my 5-year ARM (my preferred ARM term) lower before the fixed period was up. But with interest rates having moved up since I bought my house in 2014, the logical thing to do was keep holding it until the reset. The Origins Of Our 5-Year ARMWe bought a San Francisco single family fixer in 1H2014 for $1,250,000. We were tired of living in the north end of San Francisco for the past 9.5 years and wanted a change of scenery. Originally, we had planned to relocate to Hawaii, but when we found our current house with ocean views, we though this would be a good compromise. We put down 20% and took out a $992,000 5-year ARM. Originally, I was going to put down 32%, because I had about $430,000 come due from a 4.1% 5-year CD. But with a mortgage rate of only 2.5%, I felt it was worth borrowing more and investing the difference. The 2.5% mortgage rate was based on the one year LIBOR rate + a 2.25% margin – 0.25% discount for being an excellent customer. Back in 2014, the one year LIBOR rate was at only 0.5%, hence my 2.5% rate. The London Interbank Offered Rate (LIBOR) is the average interest rate at which leading banks borrow funds from other banks in the London market. LIBOR is the most widely used global “benchmark” or reference rate for short-term interest rates. Check out the historical one-year LIBOR chart below.

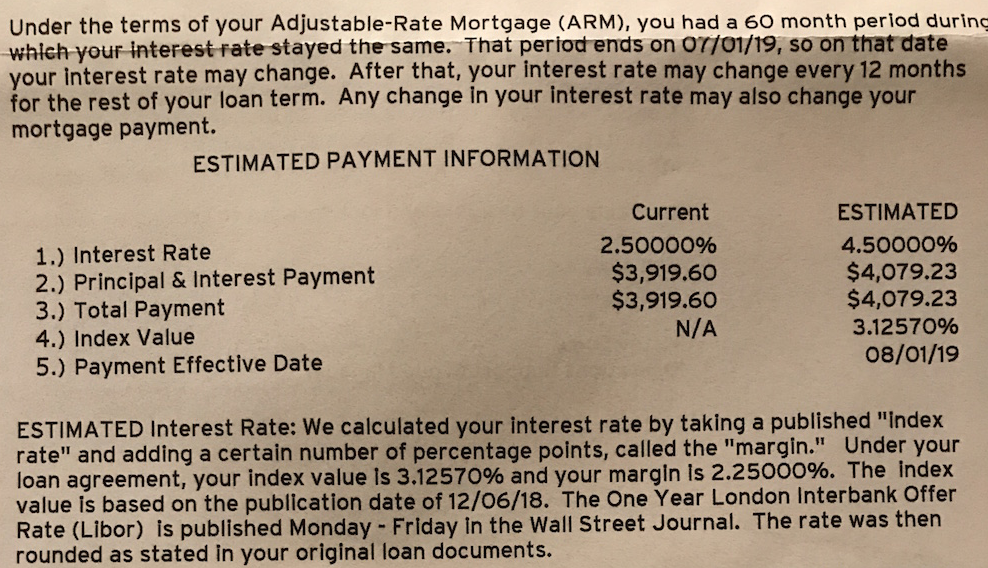

As you can tell from the one-year LIBOR chart, I bottom-ticked my mortgage rate in 2014. Some of you might be thinking that instead of getting a 5/1 ARM, I should have gotten a 30-year fixed rate instead. But given my strong belief that we will be in a permanently low interest rate environment for the rest of our lives, I felt that paying 0.85% – 1.25% more for a 30-year fixed rate was a waste of money. So my actions followed my brain. Besides, the average homeownership duration in America is only around 8.7 years. At most, one may consider taking out a 10/1 ARM to match durations. As I planned to either sell my home within 10 years in order to buy a nicer home in Hawaii or pay off the mortgage during this time frame, to me, taking out a 5/1 ARM was worth the “risk.” Regardless of whether you want to waste your money on a 30-year fixed mortgage or not, mortgage rates have indeed gone up for all of us since 2014. Based on the current one year LIBOR rate of ~3.1% + my margin of 2.25% – my 0.25% for being an excellent client, my new mortgage rate should be a reasonable 5.1% when it resets in mid-2019. If I end up paying 5.1% for the next five years, my average mortgage rate over a 10 year period would be 5.1% + 2.5% = 7.6% /2 = 3.8%. 3.8% is pretty much in-line with the rate I would have gotten if I just locked in a 30-year fixed rate mortgage in 2014. However, with the money saved from not paying a 30-year fixed mortgage and the $100,000+ less in downpayment, I ended up investing the difference and earned a ~7% return on average from 2014 – 2018 because the stock market went up until 2018. Although I did eek out a 0.8% gain in 2018. But surprise! I won't be paying an estimated 5.1% mortgage rate in 2019. Instead, my letter says that I'll be paying an estimated 4.5%. Have a look at the portion of the letter below.

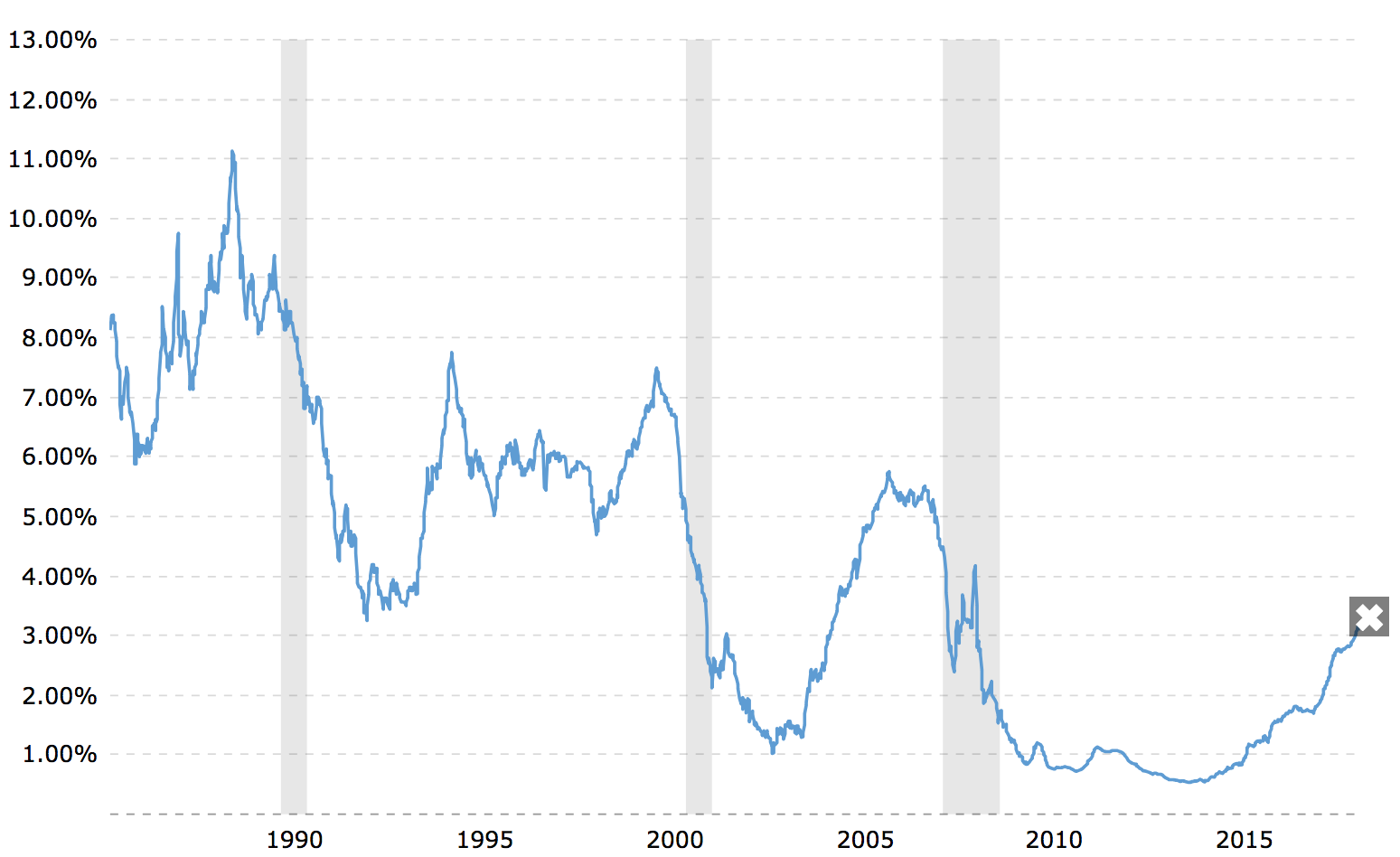

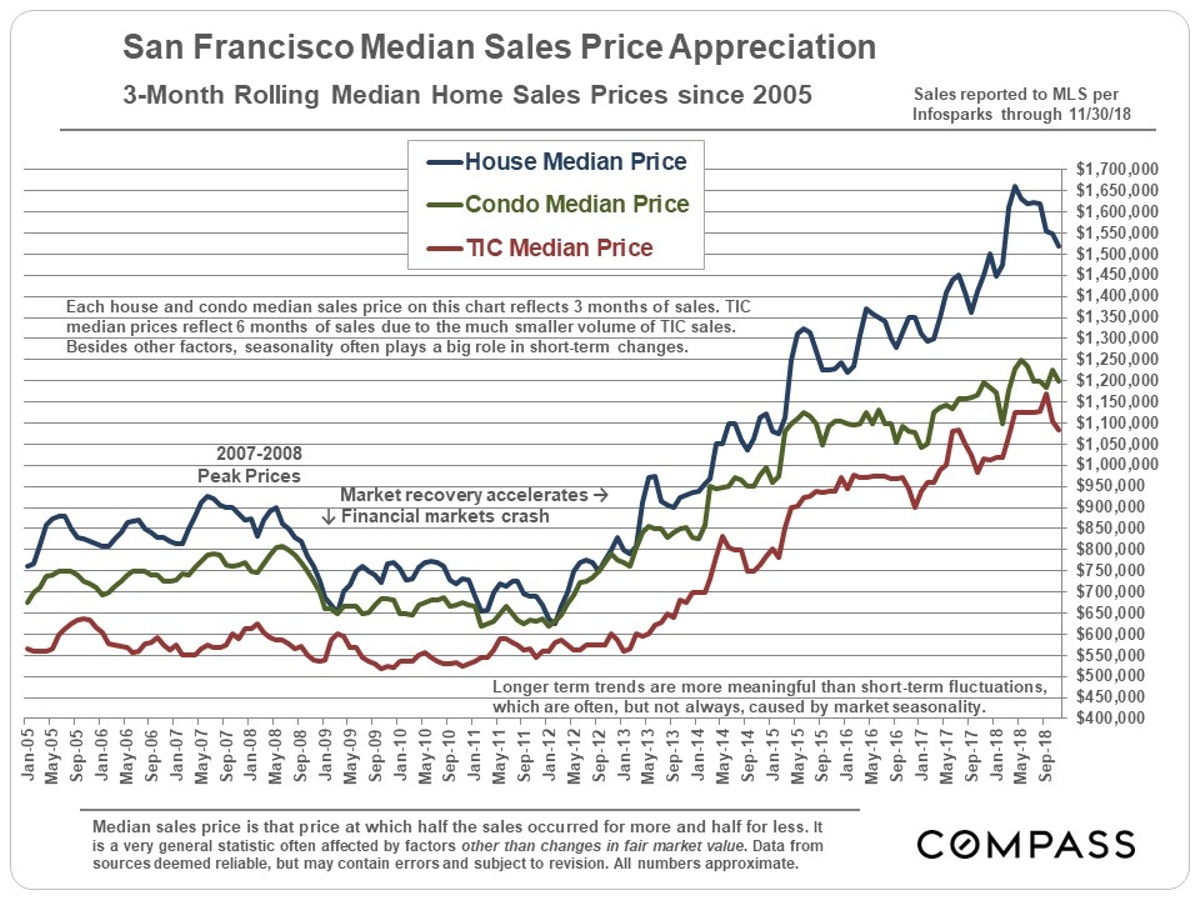

The letter clearly states how they calculate my mortgage rate, yet for some reason, they still come up with an estimated rate of 4.5% instead of 5.1%. Perhaps my good customer discount of -0.25% will grow to -0.85% next year? Or perhaps my bank simply made a mistake in their calculation. No, no. Banks aren't stupid. The reason why my rate only goes up from 2.5% to 4.5% is that under the terms of my mortgage, my ARM can only reset by at most 2% after the initial 5-year fixed rate of 2.5% is up. This maximum reset amount is pretty standard among ARM loans. But this reset amount is something you must have your bank point out in the document. The other thing to note is that ARM loans generally have a maximum mortgage interest rate they can charge for the life of your loan. In my case, that maximum is 7.5%, but we're never going to get there in my opinion. Unfortunately, after one full year at 4.5%, my bank can raise my ARM by another 2%, bringing my mortgage rate up to 6.5% for year seven. However, I doubt rates will keep on surging higher as the global economy slows. Instead, by the time my ARM reset occurs again in 7/1/2020, we might very well be in a recession with one year LIBOR rates moving back down. Paying Down PrincipalIn order to make more money, mortgage brokers and banks LOVE to scare the heck out of inexperienced homebuyers by saying their payments will surge higher once an ARM resets. They don't show them a 35-year historical chart of declining interest rates. By scaring their customers, they have a higher chance of locking them into 30-year fixed rate mortgages for fatter margins. Don't be fooled.  Historical 30-year Mortgage Interest Rate Chart You can see from the letter that despite my mortgage rate increasing from 2.5% to 4.5%, an 80% increase, my monthly payment is only expected to increase from $3,919.60 to $4,079.33, a mere 4% rise. The reason for the slight increase in monthly mortgage payment is because we've paid down 32% of our loan in 4.5 years ($992,000 down to $734,000). Paying down over $250,000 in our mortgage was partly due to normal monthly principal payments coupled with random extra principal pay downs. Although the 2.5% interest rate is low, paying down mortgage debt has always been part of my long term investment strategy. Following my FS-DAIR strategy, I would regularly try and use 25% of my free cash flow to pay down debt and use the other 75% to invest. Again, I'm just taking action based on my own advice. I kept on paying down principal randomly until the 10-year yield breached 2.5% in December 2017. Once the 10-year yield was higher than 2.5%, I stopped because I was now getting an interest-free mortgage since I could simply invest the amount of my mortgage in a 10-year bond yield to cover all my payments. Living for free is one of the best things ever! If I had taken out a 30-year fixed mortgage for 3.625%, I wouldn't have been able to experience interest-free living. Your mileage will vary in terms of how much principal you actually paid down during the initial fixed rate period of your ARM. However, even if you didn't pay down any extra principal during a five year period, you will have still paid down ~10% of your principal balance, depending on your interest rate. An Appreciation In Your Home's ValueEven if you've got to pay a higher mortgage rate when your ARM resets, you may be pleased to discover that your home has appreciated in value during the fixed rate period. The San Francisco median home price increased from $1,100,000 in 2014 to ~$1,500,000 today, or a 37% increase. A $420,000 principal increase more than makes up for a measly $159.63 monthly increase in mortgage payment, roughly half of which is going to pay down principal anyway.

Again, your home's appreciation amount will vary. Unless you timed your home purchase completely wrong, such as buying in 4Q2006 – 4Q2008 or maybe 1Q2018 (jury is still out), you'll likely come out OK. Even if you did purchase at the most recent peak, normal downturns usually last no more than 3-5 years with 10% – 20% corrections. Make A Mortgage Pay Down PlanGiven I have until 7/1/2019 before my mortgage rate jumps from 2.5% to 4.5%, I plan to keep paying my mortgage as usual and not pay anything extra to principal. As soon as I exhaust all 60 months at 2.5%, I will pay down $50,000 in principal on month 61. After the initial $50,000 extra principal payment, I will keep paying down between $20,000 – $30,000 a month in extra principal until the mortgage is gone or until I find my Hawaiian dream home. Based on my extra principal payments, the mortgage should be completely paid off by January 2022, or about 7.5 years after I first took out the loan. Anything can happen between now and January 2022, which is why it's prudent to continue investing and paying down debt while having a good cash hoard. You can now earn a healthy 2.45% in a money market account with CIT Bank, for example. That's huge, since just several years ago, savings rates were under 0.5%. Earning a 4.5% rate of return is excellent at this stage in the economic cycle, but so is having enough cash to find a gem of a property in Hawaii at a big discount. And boy, am I seeing discounts everywhere now! The alternative solution to aggressively paying down principal is to simply refinance my mortgage when it's time to reset to another 5/1 ARM. After checking online for the latest mortgage rates, I can get a 5/1 ARM jumbo for only 3.25%. This means that after 10 years, my blended interest rate is 2.875%. Not bad at all. Article Summary 1) Match the duration of your mortgage's fixed duration with the estimated ownership duration or the length of time you estimate it will take to pay off the mortgage. 2) Paying for a 30-year fixed rate mortgage might provide you more peace of mind, but you're likely overpaying for that peace of mind. 3) Read the terms of your ARM loan carefully and figure out what is the maximum interest rate increase during the first reset and what is the lifetime interest rate cap. 4) Try to make extra payments during your ARM's fixed rate period to relieve potential interest rate pressure during the reset. 5) Don't borrow more than you can comfortably afford = no greater than a 80% loan-to-value ratio with a 10% cash buffer after a 20% downpayment. Being overly leveraged is what consistently destroys people's finances. Readers, why do people take out overpriced 30-year fixed rate mortgages when the average homeownership duration is less than 9 years? Why pay a higher rate when interest rates have gone down for 35+ years in a row? The post The Anatomy Of An Adjustable Rate Mortgage Increase appeared first on Financial Samurai.

I think it is splendidly satisfying when a home reflects its owners through and through - when you walk into a home and know exactly who it belongs to without any prior debriefing. This is the complete opposite of someone who might be gregarious in their wardrobe or social pursuits, but prefers a stark and minimal home; or maybe a fun and outgoing home for an otherwise introverted person. I'm talking about the kind of home where the owner's personality is downloaded, word-for-word, into every room of the home. When this happens in design, it's downright magical. Which is why I am so enamored by the Chicago, IL home of Anna Rafferty and Richard Schreiber (and their cats Bob and Barbara). Richard is an elementary school art teacher in Chicago Public Schools, and Anna sells fantastic vintage clothes - and their affinity for creativity is plain as day. “I have a vintage clothing brand called Barbie Roadkill Vintage; I sell on Etsy as well as in a retail space that I share with two other women called Festive Collective (it's a colorful pink dreamland specializing in party supplies and vintage; you have to check it out if you're in Chicago!),” Anna begins. “I'm attracted to the bold colors and prints I grew up with in the 80s and 90s, and my vintage shop and home decorating aesthetic reflects that. My husband Richard is an elementary school art teacher, and lucky for me, he's a fan of color, too! He's content to let me handle the decorating and I'm more than happy to let him do the dishes.” Tucked onto the third (top) floor of a 1922 condo in Chicago's Lincoln Square neighborhood, Anna and Richard bought this 1,200-square-foot home in August 2018. Crayons in hand (yes, crayons), Anna got to work sketching her technicolor plans for each room. “My main goal with our home was to inject as much color into each room as possible without it looking too gaudy,” she shares. “We didn't have the budget for designer and mid-century modern furniture and decor that we love, so most of our things are secondhand from Craigslist or thrift stores, but we still sought out pieces that felt special and well-made. Ultimately, we wanted the space to feel impactful but still inviting and comfortable.” Anna's vibrant plans are now reality - with some changes and tweaks made once the couple moved into the space and really felt it out - resulting in a pleasing blend of in-your-face color, joyful accessories and vintage sensibilities. It's a home that's sure to draw out a smile. -Kelli Photography by Anna Rafferty / @barbie_roadkill & @thefestivecollective Image above: The main bedroom. Anna shares, “We hired painters before we moved in, which we've never done before and it made a huge difference to have that done first. I made sketches (on paper with crayons, I'm not tech-savvy at all) of how I thought the rooms would look, but most rooms ended up quite different once we were actually working in the space. There's only so much mapping and planning that can be done in advance; a lot of decorating is trial and error… It feels like home now, after six months, but there are still projects on my to-do list (and there probably always will be!).” Hi! I hope your year has got off to a good start? We're still in full summer-chill-mode around here. Most days I'm still in my pj's nearing lunchtime, unless it's full tide... then we're at the beach. I've also been hanging out in our veggie garden as much as I can, but more on that next week. I'm just stopping in real quick today to share this recipe, which is PERFECT for this time of the year. I shared it over on my Instagram feed at the end of last year, but it's so good I also wanted to share it here so it's easy for everyone to find in years to come. I put a call out on Instagram last week asking what kinds of things you'd like to see on here this year. Last year I sadly barely had time to even think about this space, but I'm going to try my best to change that this year (no promises, but I will try!). I'd love to hear your thoughts below in the comments, let me know the kinds of recipes you like to see, whether you'd like me to start sharing more about our veggie garden or […]

|

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

January 2019

Categories |

I'm so excited to share with you something I got in the mail the other day. No, it wasn't a notification that Financial Samurai had won an award for being the best personal finance site. My site is too focused on understanding hard things to make us all rich to appeal to the masses.

I'm so excited to share with you something I got in the mail the other day. No, it wasn't a notification that Financial Samurai had won an award for being the best personal finance site. My site is too focused on understanding hard things to make us all rich to appeal to the masses.

RSS Feed

RSS Feed